Swiss Value-add Real Estate: does it exist? should it exist?

Core, Value-add or Opportunistic real estate investments?

Classifying real estate investments into separate categories is not an easy task – real estate assets are fundamentally heterogeneous, and so are real estate investments. They differ distinctively by geography, sector, leverage usage, development exposure, business plan, risk tolerance and return objectives.

To enhance transparency in real estate markets, it has become important to attempt and sort investments into groups that are expected to share similar risk/return characteristics. This helps facilitate communication between managers, investors and other market participants, distinguish between different investment strategies, and above all, assist in transparent performance attribution and manager benchmarking.

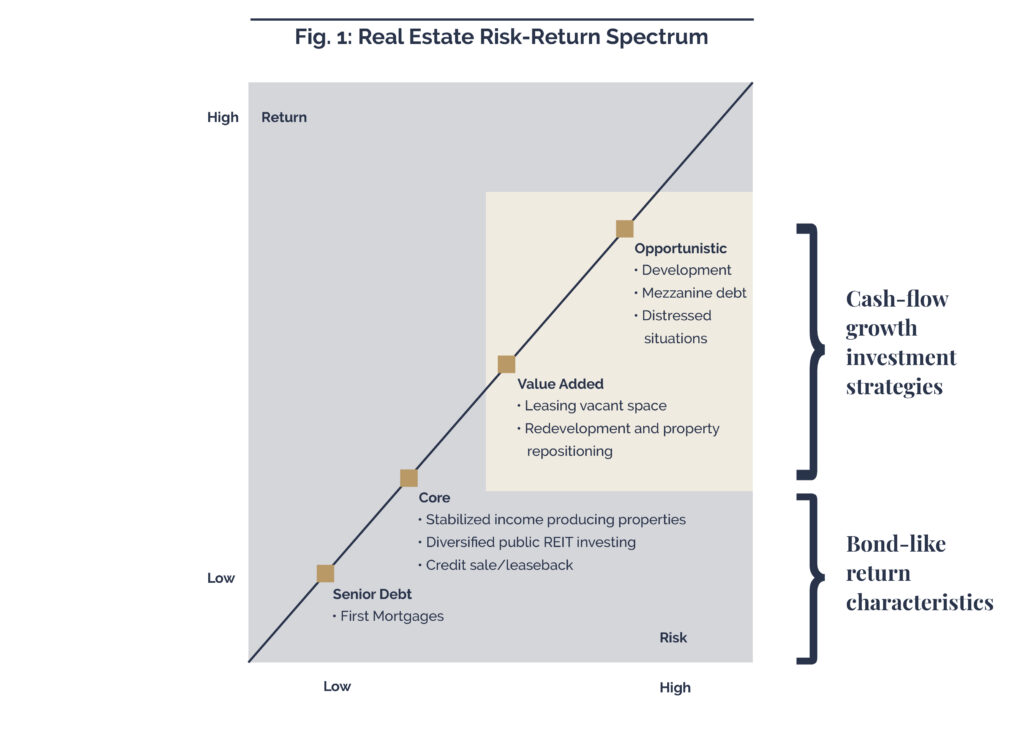

The most basic and well-established classification¹ splits real estate investments into:

- Core: investments which are mainly income producing assets. The investment typically uses low leverage, will have no or very low development exposure, and generate a high proportion of return through income.

- Value-add: investments which may be any property type and deliver returns from a balance of income return and capital appreciation. Typically, Value-add investments focus on active management, such as active leasing strategies, repositioning, or redevelopment to generate returns through adding value to the property. Value-add investments will typically use moderate leverage and on a portfolio-level might include a smaller share of developments.

- Opportunistic: investments which typically have a limited income element, use high leverage, have a high exposure to development or other forms of active asset management, and will deliver returns primarily in the form of capital appreciation. These investments may be in any markets or sectors and may be highly focused on individual markets or property types.

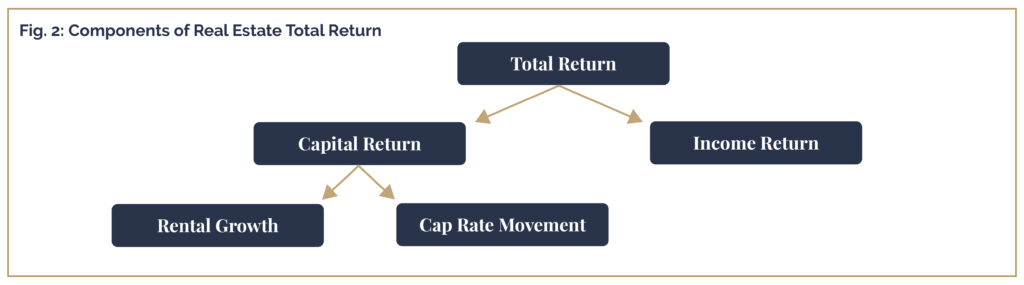

As is clear in the definitions above, the main distinction between the different strategies is the total return component on which the investment mainly focuses on. I.e. whether the investment is mainly income yield driven, or whether it targets a prominent capital appreciation return component. This decision later determines the investor’s strategy, business plan, and overall operations

The case for value-add real estate investments; in particular, Swiss value-add real estate

Value-add commercial real estate investments typically target properties with in-place cash flows and further have controllable operational upside. Such investments seek to increase such cash flows over time by making improvements to or repositioning the property. This could include making physical improvements to the asset that will allow it to command higher rents, increasing efforts to lease vacant space at the property to quality tenants, or improving the management of the property and thereby increasing customer satisfaction or lowering operating expenses where possible.

Once the income of the property has been improved or made safer/more attractive, the investor seeks to sell the asset to capture the resulting appreciation in value. Such returns are further enhanced by deploying leverage.

This approach differs significantly to a core, buy and hold, strategy in which the main return component is the income yield generated by the stable property.

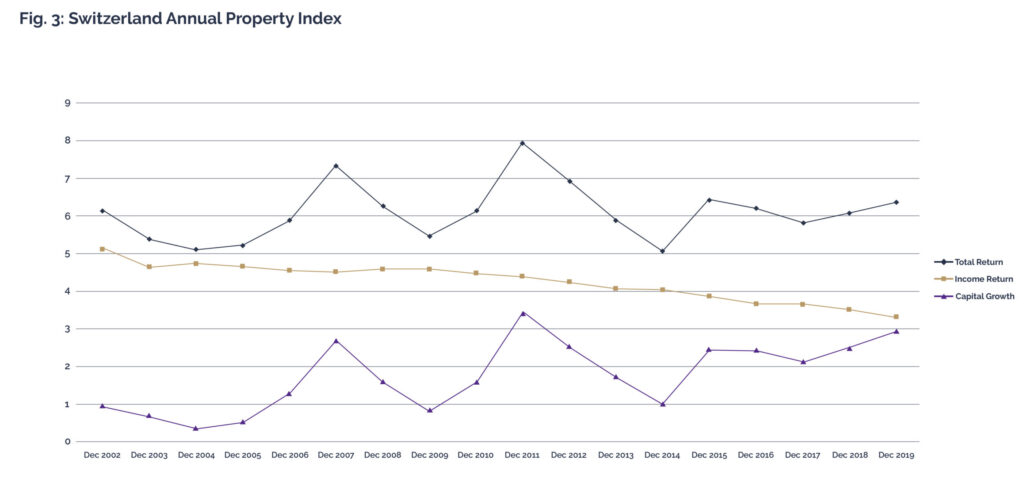

The importance of such value-creation component of total return is clearly visible when examining the total returns of Swiss real estate investments:

According to MSCI Wüest Partner data, the income return component of returns has been on a downward trend for the past 15+ years. This has mainly been driven by the availability of cheap credit and the role of Switzerland as an investment safe-haven to global investors. Such findings are even more pronounced when looking at the main geographic or sectoral markets in Switzerland such as the Zurich-office subsector where prime yields are near all-time lows (for Switzerland, and Europe as a whole).

Therefore – achieving above-market returns in Switzerland is strongly dependent on future value creation: not (only) based on market movement but through hands-on, pro-active, state-of-the-art asset management and additional capital spending (e.g. vacancy reduction, refurbishment, repositioning, re-utilization, addition of up-to-date technology features, sustainability or space expansion).

Do Swiss investors want value-add investments?

While there is not much data and research focusing on this question in Switzerland, examining basic evidence strongly supports the proposition that Swiss investors are open and interested in value-add strategies.

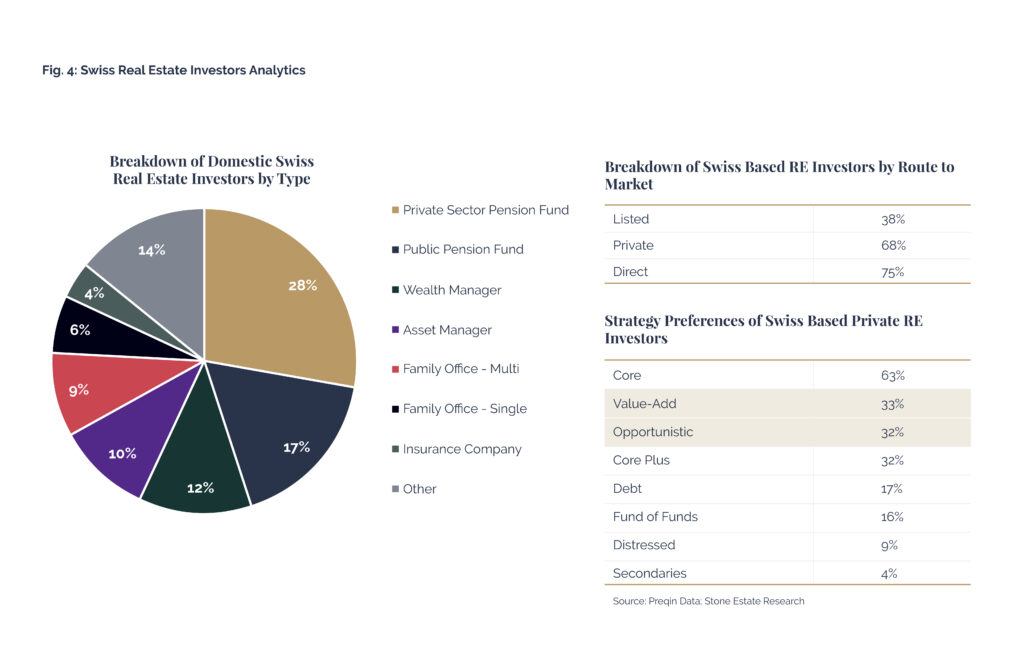

For example, according to Preqin data, 30%+ of Swiss based private real estate investors have identified value-add and opportunistic real estate investors as one of their strategy preferences. Such investors have been priced out of the core market and cannot compete with Swiss institutional capital in terms of return requirements and cost of capital.

But what about supply of professional value-add managers, do they exist?

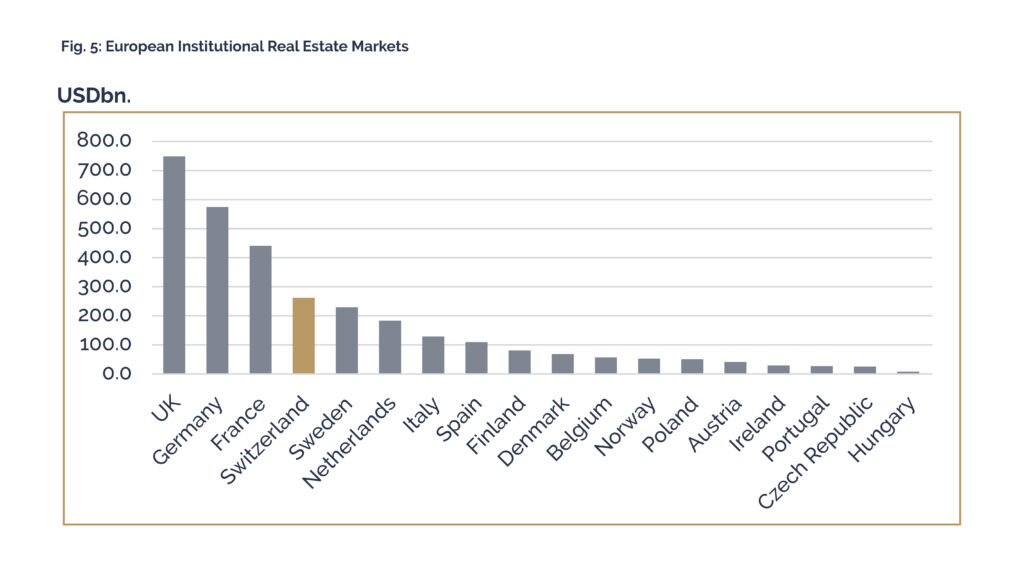

According to MSCI, Switzerland has the fourth largest institutional real estate market in Europe, worth ca. USD266.3bn

However, according to INREV, the European Association for Investors in Non-Listed Real Estate Vehicles, there are zero Swiss value-add funds or fund managers. To put those numbers in perspective, the INREV database contains information on 360+ European real estate funds, of which 71 are classified as value add – i.e. ca. 20%.

It is worth noting that of the top 5 countries, Switzerland is the only country not to have any major INREV classified value-add funds. It should also be noted that some funds classified as core have smaller allocations or verticals for value-add investments, but with only a limited number of professionals solely focussed on this market segment.

While surprising, that can mainly be attributed to Swiss real estate investors being predominantly focused on capital preservation & low yields with core representing main strategic preference.

However, as yields continue to be compressed – more and more market players are being squeezed out of the market and are actively targeting value-add strategies to achieve their return objectives.

Overall, a market imbalance exists; and more professional Value-add investment managers are needed

Currently, the market is characterized by a large number of Swiss institutions with core(+) strategies and disproportionate allocation to domestic market. The Swiss value-add & opportunistic market segments are significantly under-served with only a few experienced & sizeable players focussed on higher-yielding strategies.

However, investors have become more vocal in recent years about their interest in accessing the market through more value-creation focused investments. Such investors are interested in benefitting from both the security and safe-haven nature of Switzerland and the higher risk/return value add strategies deliver.

Moving forward, the market will likely see more players deploying a value creation approach, not (only) based on market movement but through hands-on, pro-active, state-of-the-art asset management and additional capital spending.

A market shift will occur from a buy and hold approach to one that combines, mid- to long-term income & capital value growth: growth of both, rental income and capital values (through income growth as well as yield compression based on an enhanced, repositioned product).

¹ INREV definitions